The Battle for BaaS

The Battle for BaaS

It’s Frederik here, Founder and CEO of Prospa. I’m excited to bring you Newsletter #001 of Under The Ripple. My team and I have spent time building, studying and understanding what’s happening on the ground in the Nigerian technology and business ecosystem beyond the fundraising announcements and clickbait headlines. We’ll be sharing our deep dives with you.

The inspiration for Under The Ripple came from our desire to share value with our wider community beyond our members who bank with us. We hear and see so much that it feels wrong keeping it to ourselves.

Introduction

Banking as a service (BaaS) is such a fascinating business opportunity, globally and espeically in Nigeria. In this piece, we talk about it;

Banking as a service (BaaS) is making a wave in the Nigerian fintech space.

The hook is in the 1-to-many approach it offers vs. the direct-to-consumer approach, and the ability to scale fast.

Beyond new startups, who are the established players?

Collaboration or competition?

BaaS and Telcos

BaaS and e-commerce

Cards as a Service and it’s promise

Achieving scalability and obstacles.

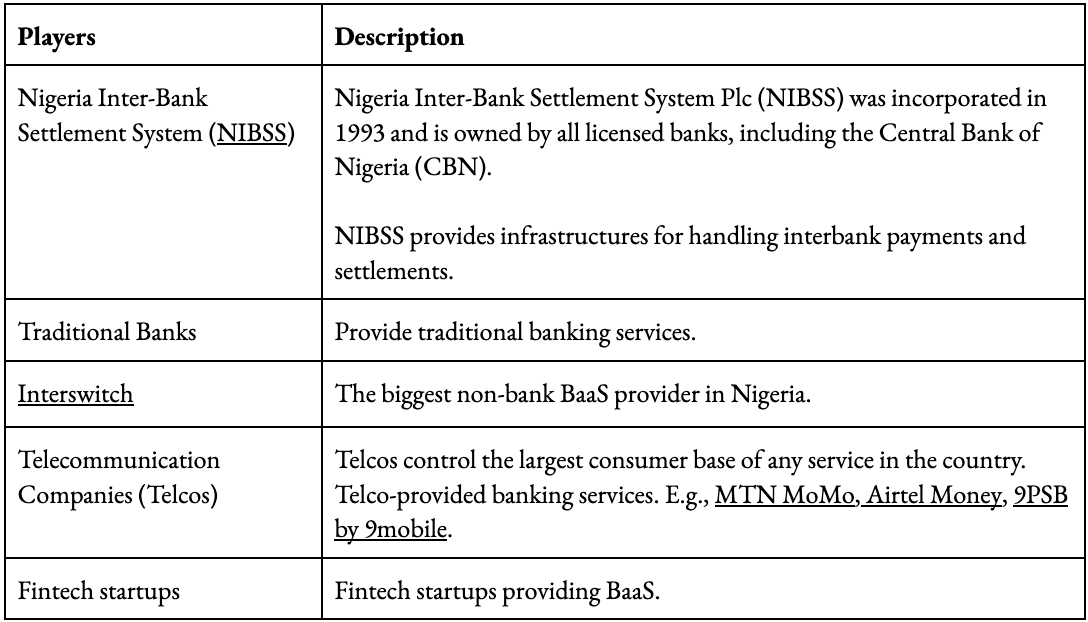

Key players

Before we dive in, let’s establish some of the players in the Nigerian BaaS space. We’ve split the companies into three categories.

Market leaders - By revenue, size and scale of business e.g. Interswitch, e-transact

Established innovators - Well-funded, matured businesses, e.g., Paystack, Flutterwave

New entrants - Tech startups, typically early-stage

The services

It is important we qualify what we are talking about. When we say banking as a service, we refer to the decoupling of services traditionally provided by commercial banks, banking institutions and non-bank financial institutions. Just like other leading and emerging markets, Nigerian BaaS providers have also segmented and zoned in on one or more service areas.

The opportunity

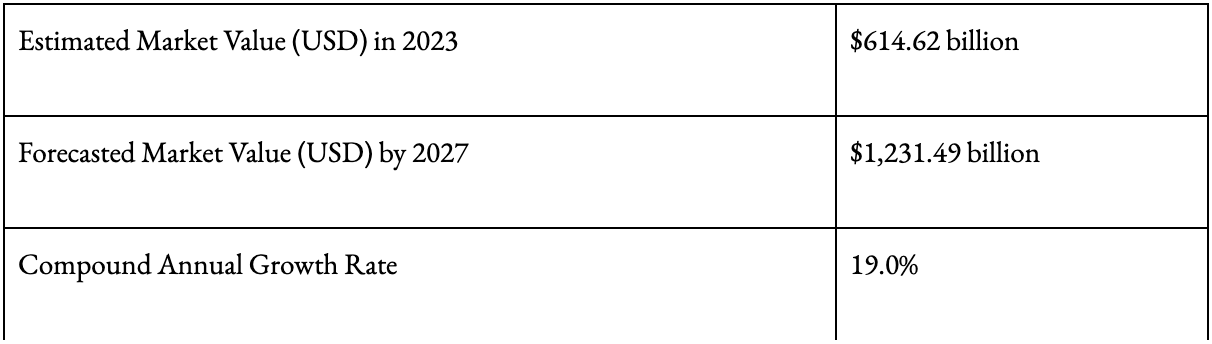

Let’s be honest: We don’t know definitively the value or true size of the BaaS market in Nigeria, but there are some simple building blocks that can help us understand the scale of the opportunity.

Global estimate BaaS and looking at it’s growth rates

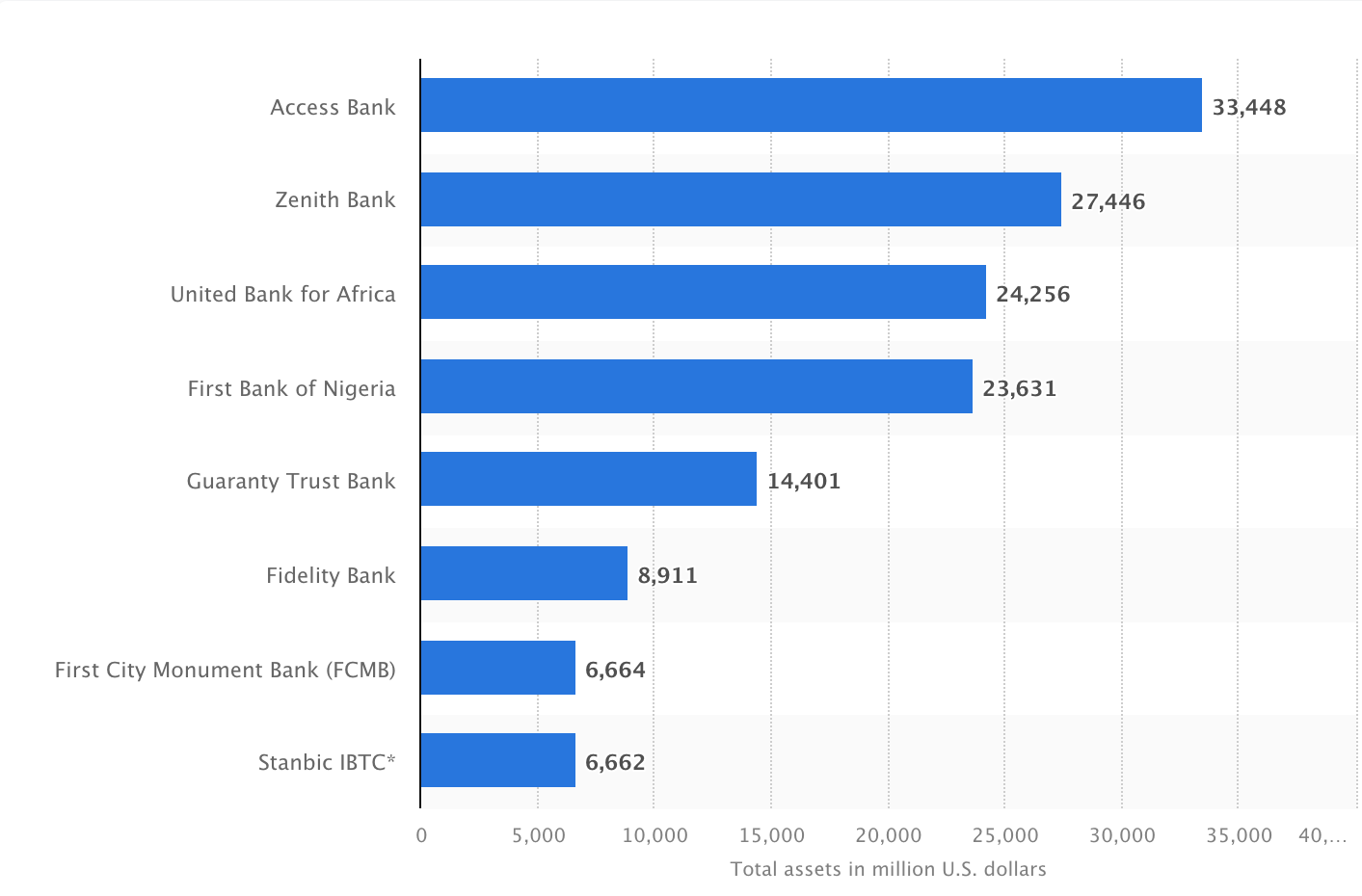

The assets/value of top commercial banks indicates the size of the opportunity. The thinking block here is that Nigeria’s top commercial banks, to a large extent, have realised the value of a direct-to-market approach and been able to monetise payments at a large scale across multiple services, e.g., transfers, wallets, cards, KYC (Number of accounts), etc. This can be used as an indication of the underlying value of the market in Nigeria.

From the number of entrepreneurs launching new BaaS startups, existing traditional banks decoupling existing services and repackaging them as fintech startups, large organisations acquiring the necessary licences to provide banking services, it is clear that a large opportunity exists.

BaaS & Telcos

The telecoms industry in Nigeria is important and has done a lot of work over the years to capture value from a large subscriber base. For BaaS providers, the Telcos presented an opportunity to partner and open a large consumer base to a range of financial services, capturing the commercial opportunity along with that.

The pitch seems to be simple, BaaS provider X partners with MTN and provides the financial service infrastructure, MTN provides the network and distribution and they ride off into the sunset with billions of dollars. But what we see Under the ripple is different. Telcos initially partner with BaaS providers and gain learnings in the initial phases, but prefer to build their own infrastructure when it's time to scale. Creating subsidiaries or new “fintech” divisions, raising fresh capital and aggressively pursuing the opportunity.

Circa 2022, the telecommunications giant MTN launched its MoMo Payment Service Bank (PSB), offering banking services to 76.7+ million customers. Prior to that time, its payment system was powered by Interswitch.

Remember our three categories of companies, where new entrants are concerned it is very difficult to pull off a partnership of real significance with a large Telco. The Telcos are cutting ties with established BaaS market leaders and emerging innovators and going solo. They have the capital, existing market, distribution channels and critical licensing to go solo. Under the ripple, we actually see that the telcos are turning BaaS and powering New entrant Fintechs who then resell or wholesale these services to other fintechs.

BaaS has provided fintech startups with the opportunity to create specialised products like ChipperCash and Grey Finance for forex needs. Airtel’s SmartCash, however, already allows Nigerians to receive foreign currency directly into their wallets, while MTN’s MoMo allows Nigerians to send and receive money across several African countries, competing with the likes of Send by Flutterwave and ChipperCash. The PSB licence permits global wallets and remittances by default; a very advantageous facet of the licence.

BaaS & E-commerce

Again, just like telcos, e-commerce seemingly presents an opportunity for BaaS providers to partner with companies that seem like an instant fit and provide the opportunity to scale from one to many. But again, under the ripple, we see something a bit different.

Companies like Jumia and Konga also started off employing BaaS to provide financial services to their customers and later went on to build their own financial infrastructure as they scaled, namely JumiaPay and KongaPay, respectively. In the case of Konga, this article by Quartz Africa shows that these changes were born out of necessity as a result of the high failure rates experienced with these integrations as far back as 2016. However, with a more refined and efficient solution and higher success rates, Jumia has repeatedly switched between Interswitch and Paystack integrations and eventually launched its own financial infrastructure (JumiaPay) in 2016, offering loans, investments and other financial services on the JumiaPay app.

These cases corroborate that, although the move to build their own infrastructure was born out of necessity in the early days, these organisations have realised the potential revenue lost from integrating BaaS and the underutilisation of their customer network as they scale.

As organisations scale, they become less inclined to partner and more inclined to build their own infrastructure.

B2B e-commerce platform TradeDepot also recognised the importance of embedding finance into its products, and as its network of 40,000 micro retailers grows, it could go on to offer banking services. So, there is promise in approaching existing companies, but how many of them are using third parties?

BaaS and Banks - Collaborating and Competing

The relationship between commercial banks and BaaS is very interesting and comes with both collaboration and competition, as banks are aggressively trying to compete with fintech startups. Both offer the same products, the only difference being cost and ease. Providus and Wema Bank are some of the first legacy banks to create BaaS products for fintechs and have contributed significantly to the growth of the fintech industry. However, Legacy banks have the advantage of branding and economies of scale. They can compete with BaaS and BaaS-integrated startups if they choose to, as seen with ALAT, a digital banking product by Wema Bank, which launched in May 2017 and acquired 250,000 customers in its first year. Leveraging on existing customers, Squad by GTBank was launched in 2022 to compete with the likes of Monnify (by Monieepoint), Paystack and Flutterwave in terms of pricing, as they all provide payment gateways, POS, and e-commerce. While traditional banks have supported BaaS providers, Some banks like Providus have more recently begun creating BaaS products themselves.

As New entrant BaaS providers like Anchor, Maplerad, Bloc, Parkway and OnePipe compete for new and existing businesses, there may be a conundrum with retention as these businesses scale. While they provide easy integration, platforms will likely integrate directly with banks as they scale, and may eventually build their own infrastructure. The benefits they provide to smaller platforms, however, can not be ignored. A good market case would be for BaaS providers to avoid limiting services to fintech, FMCG, and travel/mobility, as the promise of BaaS is not restricted to these verticals. The search for new verticals becomes ever more important for new entrants looking to build large-scale ventures.

Cards as a service (CRDaaS)

Cards issuing and acquiring, even as a neobank, has been a long and difficult process. The issue with launching cards is that every card issuance scheme requires a settlement bank, which can be slow to integrate. For physical cards, an integration partner may also sit in-between the settlement bank and the card network. Interswitch dominates market share with its own indigenous card network (Verve), as well as serving as a main integration partner for the global card networks and a service provider for legacy banks. However, startups like Blusalt are reportedly launching new services in this space, with direct integrations and speedy set-up.

While there may be a lot of promise for Cards as a Service (CRDaaS) startups, we are yet to experience a startup truly provide seamless integration to launch a reliable physical or virtual card program. In our journey to launch Prospa cards, we spent ~2 years finding the right combination of licensing, direct relationship with the network, and aggressive and sometimes chaotic follow-up with our traditional settlement bank. In surveying the market, we have attempted to request physical cards from almost every fintech in the market, and have a higher failure rate than success rate. “Coming soon” seems to be a popular word, and we understand. The opportunity here, no doubt, is huge, but it will require deep relationships with the card networks, technical excellence and a regulatory environment to support all the innovation required for a thriving CRDaaS market.

Conclusion

In Nigeria, the already dominant companies are nimble and aggressive. It’s not unlikely the BaaS market will be won by established players; Interswitch, e-transact, and commercial banks like Access, Wema and Providus. New entrants face the challenge of scale, as would-be partners with the large end-user bases usually opt to establish their own infrastructure when extending financial services to them. Established innovators will eventually partner with the tier 2 banks, as seen in the partnership between Paystack and Titan Trust Bank. New entrants will have to find their feet, and one way they could do that is to niche down to specific markets.

Good Reads

Airtel’s PSB, SmartCash now allows Nigerians to receive remittances into their mobile money wallets

Africa’s 4 $1b fintech unicorns could pave the way for startups

Why your favourite online savings platform is giving you a virtual account number

How GTCO’s fintech firm squares up to competition - Businessday NG

Fintech giant Interswitch eyes telecoms market with $1 million MNVO license